Note

Go to the end to download the full example code.

Example: Holt-Winters Exponential Smoothing

In this example we show how to implement Exponential Smoothing. This is intended to be a simple counter-part to the Time Series Forecasting notebook.

The idea is that we have some times series

where we train on \(y_1, ..., y_T\) and predict for \(y_{T+1}, ..., y_{T+H}\), where \(T\) is the maximum training timestamp and \(H\) is the maximum number of future timesteps for which we want to forecast.

We will be using the update equations from the excellent book Forecasting Principles and Practice:

where

\(\hat{y}_t\) is the forecast at time \(t\);

\(h\) is the number of time steps into the future which we want to predict for;

\(l_t\) is the level, \(b_t\) is the trend, and \(s_t\) is the seasonality,

\(\alpha\) is the level smoothing, \(\beta^*\) is the trend smoothing, and \(\gamma\) is the seasonality smoothing.

\(k\) is the integer part of \((h-1)/m\) (this looks more complicated than it is, it just takes the latest seasonality estimate for this time point).

import argparse

import os

import time

import matplotlib

import matplotlib.pyplot as plt

import numpy as np

import jax

from jax import random

import jax.numpy as jnp

import numpyro

from numpyro.contrib.control_flow import scan

from numpyro.diagnostics import hpdi

import numpyro.distributions as dist

from numpyro.infer import MCMC, NUTS, Predictive

matplotlib.use("Agg")

N_POINTS_PER_UNIT = 10 # number of points to plot for each unit interval

def holt_winters(y, n_seasons, future=0):

T = y.shape[0]

level_smoothing = numpyro.sample("level_smoothing", dist.Beta(1, 1))

trend_smoothing = numpyro.sample("trend_smoothing", dist.Beta(1, 1))

seasonality_smoothing = numpyro.sample("seasonality_smoothing", dist.Beta(1, 1))

adj_seasonality_smoothing = seasonality_smoothing * (1 - level_smoothing)

noise = numpyro.sample("noise", dist.HalfNormal(1))

level_init = numpyro.sample("level_init", dist.Normal(0, 1))

trend_init = numpyro.sample("trend_init", dist.Normal(0, 1))

with numpyro.plate("n_seasons", n_seasons):

seasonality_init = numpyro.sample("seasonality_init", dist.Normal(0, 1))

def transition_fn(carry, t):

previous_level, previous_trend, previous_seasonality = carry

level = jnp.where(

t < T,

level_smoothing * (y[t] - previous_seasonality[0])

+ (1 - level_smoothing) * (previous_level + previous_trend),

previous_level,

)

trend = jnp.where(

t < T,

trend_smoothing * (level - previous_level)

+ (1 - trend_smoothing) * previous_trend,

previous_trend,

)

new_season = jnp.where(

t < T,

adj_seasonality_smoothing * (y[t] - (previous_level + previous_trend))

+ (1 - adj_seasonality_smoothing) * previous_seasonality[0],

previous_seasonality[0],

)

step = jnp.where(t < T, 1, t - T + 1)

mu = previous_level + step * previous_trend + previous_seasonality[0]

pred = numpyro.sample("pred", dist.Normal(mu, noise))

seasonality = jnp.concatenate(

[previous_seasonality[1:], new_season[None]], axis=0

)

return (level, trend, seasonality), pred

with numpyro.handlers.condition(data={"pred": y}):

_, preds = scan(

transition_fn,

(level_init, trend_init, seasonality_init),

jnp.arange(T + future),

)

if future > 0:

numpyro.deterministic("y_forecast", preds[-future:])

def run_inference(model, args, rng_key, y, n_seasons):

start = time.time()

sampler = NUTS(model)

mcmc = MCMC(

sampler,

num_warmup=args.num_warmup,

num_samples=args.num_samples,

num_chains=args.num_chains,

progress_bar=False if "NUMPYRO_SPHINXBUILD" in os.environ else True,

)

mcmc.run(rng_key, y=y, n_seasons=n_seasons)

mcmc.print_summary()

print("\nMCMC elapsed time:", time.time() - start)

return mcmc.get_samples()

def predict(model, args, samples, rng_key, y, n_seasons):

predictive = Predictive(model, samples, return_sites=["y_forecast"])

return predictive(

rng_key, y=y, n_seasons=n_seasons, future=args.future * N_POINTS_PER_UNIT

)["y_forecast"]

def main(args):

# generate artificial dataset

rng_key, _ = random.split(random.key(0))

T = args.T

t = jnp.linspace(0, T + args.future, (T + args.future) * N_POINTS_PER_UNIT)

y = jnp.sin(2 * np.pi * t) + 0.3 * t + jax.random.normal(rng_key, t.shape) * 0.1

n_seasons = N_POINTS_PER_UNIT

y_train = y[: -args.future * N_POINTS_PER_UNIT]

t_test = t[-args.future * N_POINTS_PER_UNIT :]

# do inference

rng_key, _ = random.split(random.key(1))

samples = run_inference(holt_winters, args, rng_key, y_train, n_seasons)

# do prediction

rng_key, _ = random.split(random.key(2))

preds = predict(holt_winters, args, samples, rng_key, y_train, n_seasons)

mean_preds = preds.mean(axis=0)

hpdi_preds = hpdi(preds)

# make plots

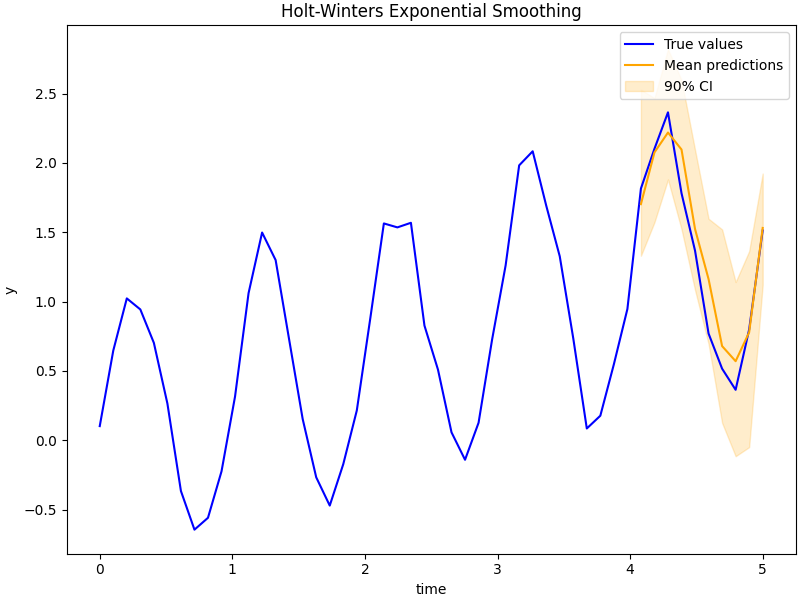

fig, ax = plt.subplots(figsize=(8, 6), constrained_layout=True)

# plot true data and predictions

ax.plot(t, y, color="blue", label="True values")

ax.plot(t_test, mean_preds, color="orange", label="Mean predictions")

ax.fill_between(t_test, *hpdi_preds, color="orange", alpha=0.2, label="90% CI")

ax.set(xlabel="time", ylabel="y", title="Holt-Winters Exponential Smoothing")

ax.legend()

plt.savefig("holt_winters_plot.pdf")

if __name__ == "__main__":

assert numpyro.__version__.startswith("0.21.0")

parser = argparse.ArgumentParser(description="Holt-Winters")

parser.add_argument("--T", nargs="?", default=6, type=int)

parser.add_argument("--future", nargs="?", default=1, type=int)

parser.add_argument("-n", "--num-samples", nargs="?", default=1000, type=int)

parser.add_argument("--num-warmup", nargs="?", default=1000, type=int)

parser.add_argument("--num-chains", nargs="?", default=1, type=int)

parser.add_argument("--device", default="cpu", type=str, help='use "cpu" or "gpu".')

args = parser.parse_args()

numpyro.set_platform(args.device)

numpyro.set_host_device_count(args.num_chains)

main(args)